OECD minimum tax

Switzerland introduced the minimum tax proposed by the Organisation for Economic Co-operation and Development (OECD) on 1 January 2024. It has a severe impact on Switzerland and its financial centre as an export-oriented country with moderate taxation and a small domestic market.

The OECD minimum tax became a new global tax standard in 2024. It was agreed by around 140 states, including Switzerland. The new rules state that a minimum tax rate of 15% is to be applied to profits of multinational enterprises. This means a higher tax bill for large companies in Switzerland as of 2024, since the tax rate in many cantons was previously below 15%. Nothing has changed for all other, smaller companies. Introducing the OECD minimum tax rate required a change to the Constitution.

This also affects the financial centre. The banks in Switzerland support the introduction of the OECD minimum tax, even though it equates to a tax hike. Under the mechanism worked out by the international community, a failure on Switzerland’s part to adjust its tax system would have resulted in other states being able to impose additional taxes on companies in Switzerland. In other words, companies have to pay at least 15% tax, whatever happens. The extra tax revenues would thus have flowed to foreign states if Switzerland had not implemented the OECD minimum.

How does the OECD minimum tax work?

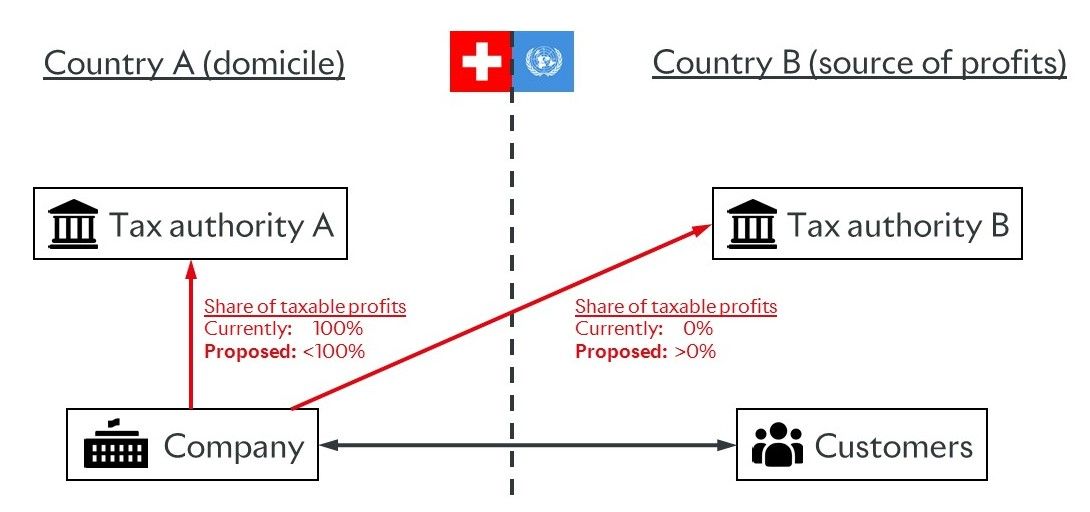

The new rules are divided into two pillars. Pillar One essentially covers the cross-border profits of companies with total revenues of more than EUR 20 billion and a profit margin of more than 10%. This means that a company based in one country (Country A) can be taxed in another (Country B) on the profits it makes there, even if it has no physical presence in that country. As regulated financial service providers, banks are exempt from Pillar One, as is the mining industry.

{kind=link}

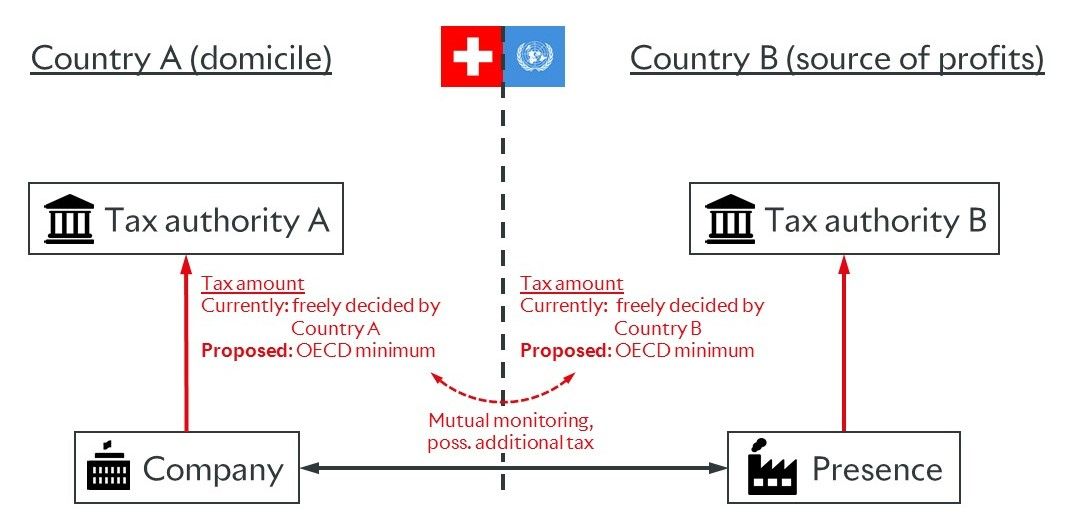

Pillar Two covers the cross-border profits of corporations with total revenues of more than EUR 750 million. Their profits are now taxed at a rate of at least 15%. Pillar Two is independent from Pillar One.

{kind=link}

Legal implementation of Pillar Two in Switzerland

On 18 June 2023, the Swiss electorate voted in favour of a change to the Constitution that created the legal basis for implementing the minimum tax in Switzerland. One of the legislator’s aims was to ensure that the revenues from this higher taxation remain in Switzerland rather than flowing to other countries.

A new transitional provision in the Constitution provides the Federal Council with a framework for implementing the minimum tax, which it decided to do by introducing a national top-up tax with effect from 1 January 2024. In September 2024, the Federal Council decided that it would also introduce an international top-up tax under the Income Inclusion Rule (IIR) with effect from 1 January 2025. It issued a Minimum Tax Ordinance to this effect. This remains in force until replaced by a federal law, which the Federal Council must present to the Swiss Parliament within six years.

International progress in implementation

No country has yet implemented Pillar One. Pillar Two has so far been introduced by the EU, the UK, Canada, Australia, Japan and South Korea. Implementation by other countries with economic importance for Switzerland, such as the US, China and the BRIC states, is uncertain or unlikely, especially since the US government has expressly opposed it since January 2025.